$5M Citibank Account CLOSED Over Coinbase Transfer Can Trump’s Order Stop Debanking?

Key Takeaways

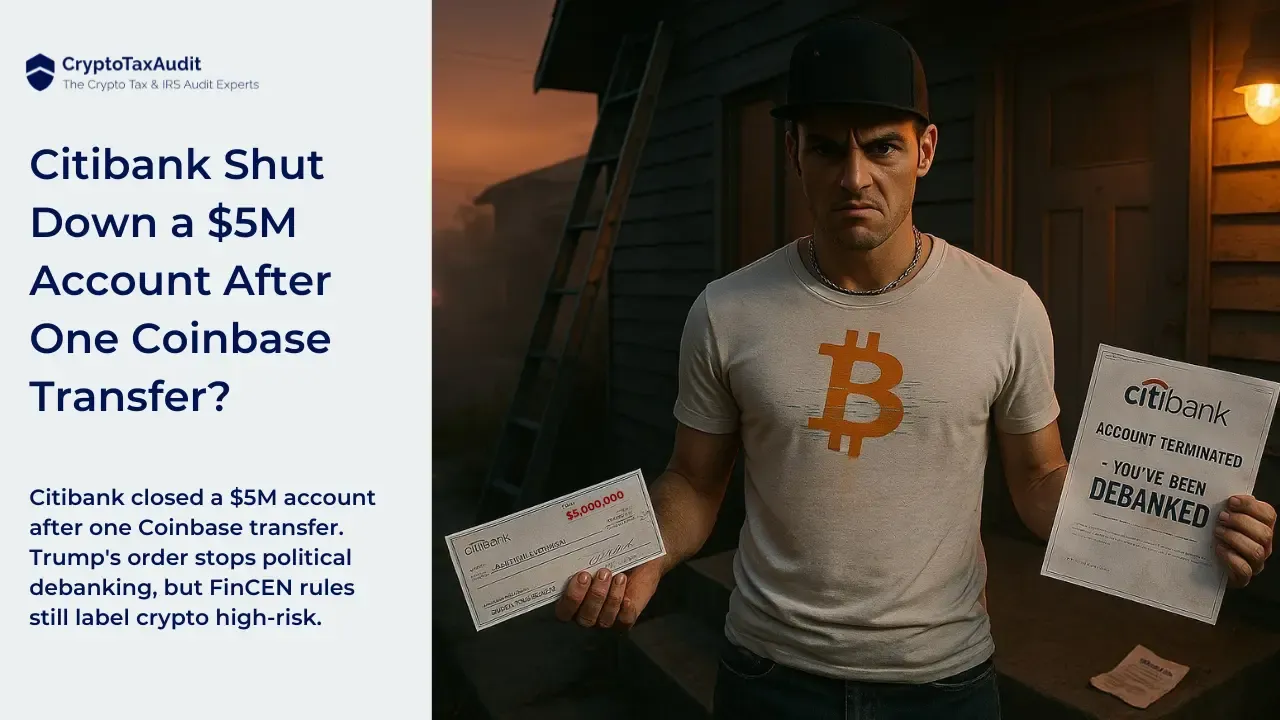

- A client lost access to his $5 million Citibank account after transferring funds from Coinbase.

- Trump’s new executive order targets political “debanking” but leaves crypto users exposed.

- FinCEN rules still label crypto transactions as high risk, requiring extra due diligence on clients.

- Until FinCEN changes its stance, crypto investors remain at risk of being denied transaction by their bank.

What Really Happened When a $5 Million Account Was Closed?

A client of mine once wired $1 million from Coinbase into his Citibank account.

Citibank rejected the transfer and then shut his account no warning, no discussion.

They mailed him a check for the full $5 million balance.

Can you imagine a $5 million check floating through the mail?

That’s what debanking looks like in the crypto world: one transaction and you’re gone.

What Is “Debanking” and Why Is Trump Trying to Stop It?

In August 2025, President Trump issued an executive order designed to stop banks from closing accounts for political or ideological reasons.

He and his sons were debanked themselves, so he’s familiar with the problem.

The order says banks must stay apolitical, they can’t shut down accounts as punishment for someone’s beliefs or associations.

That’s progress, but it doesn’t fix the main issue facing crypto investors.

Banks can still close your account if they suspect you’re involved in illegal activity. They are free to deny your transaction if they feel it’s too risky.

And thanks to FinCEN’s rules, crypto transactions are automatically treated as “high risk.”

Why FinCEN’s Rules Still Make You a Target

FinCEN the Financial Crimes Enforcement Network runs America’s anti–money-laundering system.

It requires banks to treat every crypto-related transaction with the highest level of scrutiny.

That means enhanced due diligence every time crypto money hits a traditional account.

On average, a single review can take six hours of staff time. Most banks don’t want the cost of compliance risk.

So they take the easy route: they deny transactions.

This creates a back-door ban on crypto. You might never break a law, but the compliance burden makes you too “expensive” to keep as a customer.

The Global Pressure Behind FinCEN’s Policy

FinCEN didn’t invent these restrictions alone.

They’re following guidance from the Financial Action Task Force (FATF), an international body tied to the IMF.

The FATF pushed every country to classify crypto as a high-risk asset for money laundering.

That global coordination means even if Trump tells U.S. banks to stop political debanking, FinCEN can still keep crypto users in the crosshairs under AML rules.

It’s a policy problem at the root not just political censorship.

The Hypocrisy: Cash, Not Crypto, Is the Real Money-Laundering Tool

Let’s get real.

Most money laundering happens in cash, not crypto.

Crypto leaves a permanent digital trail, it’s traceable.

Cash doesn’t.

Yet regulators treat crypto as the bigger threat.

That’s an irrational policy.

If the U.S. wants to lead the blockchain economy, it must tell FinCEN to stop treating crypto like contraband.

What Needs to Change

The fix isn’t just an executive order.

The administration must pressure FinCEN to drop its blanket “high-risk” stance and push back on FATF.

If crypto transfers are handled like normal financial activity, banks would have no excuse to close accounts.

Until that happens, investors should assume the risk is still there.

One flagged transfer can increase your risk of more flagged transfers.

What You Can Do Right Now

If you hold or trade crypto, protect yourself before the bank does it for you.

- Keep separate bank accounts for crypto activity.

- Maintain documentation showing the source of your funds.

- If your exchange transfer gets blocked, don’t re-send it ask your tax or legal advisor first.

And most importantly, get professional help before the IRS or FinCEN start asking questions.

At CryptoTaxAudit.com, our team helps clients document crypto transactions, defend against IRS audits, and prepare for banking reviews.

We’ve beaten the IRS on analytics before — we know how to defend crypto investors.

Related: 1099-DA Crypto Reporting: What the IRS Will Track in 2026

Frequently Asked Questions About Crypto Taxes

Q1: Can a bank still close my account because of crypto?

A: Yes. The executive order limits political debanking, not anti-money-laundering enforcement.

If your activity looks risky to the bank, they can still offboard you.

CryptoTaxAudit helps clients document transactions to reduce that risk.

Q2: What’s FinCEN’s role in debanking?

A: FinCEN enforces anti-money-laundering policy.

Its guidance tells banks to treat crypto transfers as high risk, triggering extra due diligence.

CryptoTaxAudit tracks these regulations and prepares clients for reviews or audits.

Q3: Does Trump’s order protect routine Coinbase or exchange transfers?

A: Not directly.

Until FinCEN updates its rules, banks may still flag or reject exchange transfers.

CryptoTaxAudit can help you present clear, compliant records to your bank.

Q4: If I get debanked, can I fight it?

A: You can file a complaint with your regulator—usually the Office of the Comptroller of the Currency (OCC)—but success rates are low.

CryptoTaxAudit assists clients in documenting legitimacy and rebuilding compliant banking relationships.

Q5: Could debanking trigger IRS attention?

A: Yes. Banks may file Suspicious Activity Reports with FinCEN or the IRS when they close crypto accounts.

Having organized records and cost-basis documentation protects you.

CryptoTaxAudit defends clients under IRS scrutiny.

Q6: What records should I keep to protect myself?

A: Keep every trade, transfer, and wallet move—plus fiat on- and off-ramps.

The IRS expects precise digital asset records.

CryptoTaxAudit helps clients build audit-ready systems for long-term protection.

Q: Where can I learn more about FinCEN’s crypto guidance?

A: Read FinCEN’s advisory on “Convertible Virtual Currencies” at FinCEN.gov.

Then visit CryptoTaxAudit.com to see how we can help protect your portfolio.

Author