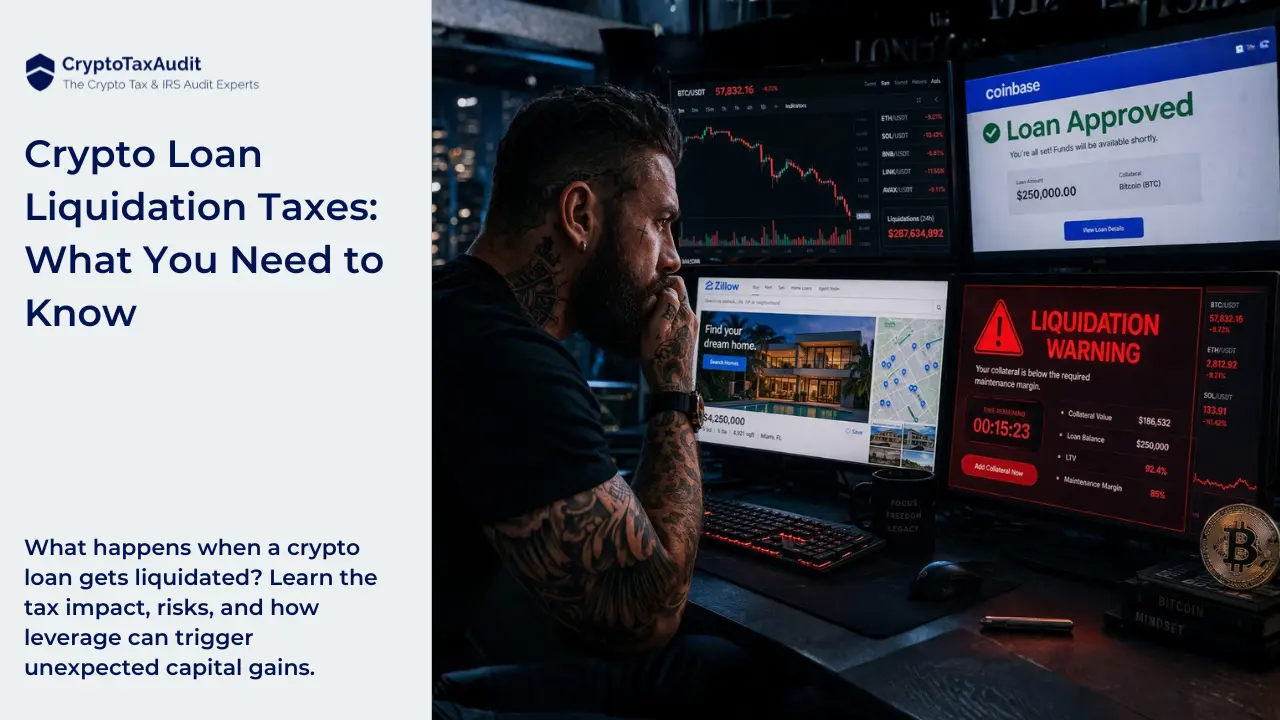

What Happens If a Crypto Loan Gets Liquidated? Taxes, Risk, and Leverage Explained

By Clinton Donnelly, CEO, Founder | CryptoTaxAudit

Coinbase has partnered with Better Homes and Finance Holding Company to let crypto owners use their holdings as collateral for a mortgage down payment.

Instead of selling crypto and triggering capital gains, borrowers can take out a cash loan against their holdings. The asset stays in place. The loan provides the liquidity.

It sounds clean. It isn't.

What most borrowers don't consider is what happens if crypto prices fall sharply while that loan is outstanding.

If the collateral drops below a required threshold, the lender liquidates it automatically. That liquidation is a taxable event.

The borrower owes capital gains tax on assets they no longer own, at a price they didn't choose.

This post explains how crypto-backed loans work, when and why liquidation occurs, what the tax consequences are, and how to think about the risk before committing to a leveraged position.

Key Takeaways

- Crypto loan liquidation is a capital gains tax event. When a lender sells your crypto collateral to satisfy a loan, the IRS treats that sale the same as if you sold it voluntarily. You owe tax on the gain regardless of whether you received any proceeds.

- The taxable proceeds equal the outstanding loan balance at the time of liquidation. The sale price on your crypto is recorded as the current value of what you owed, not necessarily what the collateral was worth when you put it up.

- Borrowing against Bitcoin creates a leveraged position. If Bitcoin drops, you don't just lose value on the asset. You still owe the loan. That combination can result in losses that exceed the original collateral value.

- Typical loan-to-value ratios require 2x to 3x collateral. To borrow $100,000 in a stablecoin, you may need to post $200,000 to $300,000 in cryptocurrency. This provides a buffer but doesn't eliminate liquidation risk in a severe downturn.

- Capital gains tax on liquidated crypto can range from 20% to 30% or more. Federal capital gains rates plus state taxes mean a forced liquidation event can result in a substantial tax bill at the worst possible moment financially.

How Crypto-Backed Loans Work

A crypto-backed loan lets you borrow cash against cryptocurrency you already own without selling it. The crypto is posted as collateral.

The lender holds it while the loan is outstanding. You receive a cash disbursement, typically in a stablecoin or fiat.

The loan-to-value (LTV) ratio determines how much you can borrow relative to the collateral you post. Most crypto lenders require $200,000 to $300,000 in crypto to secure a $100,000 loan.

That ratio gives the lender a cushion if prices fall.

The appeal is straightforward. If Bitcoin averages 15% annual growth and you're only paying 6% annual interest on the loan, you net a 9% return on an asset you haven't sold.

The asset continues to appreciate while the loan covers your immediate cash need. The risk is equally straightforward. That math reverses fast if the asset drops instead of rises.

What Is a Liquidation Event?

Liquidation happens when the value of your crypto collateral falls below the lender's required threshold. At that point, the lender sells your crypto automatically to recover what you owe.

You don't make the decision. You don't choose the timing or the price.

The loan agreement defines the liquidation threshold. If you posted $200,000 in Bitcoin to secure a $100,000 loan, you could typically withstand a 50% drop in Bitcoin's price before hitting the liquidation trigger.

Below that threshold, the collateral is sold.

The mechanics are automatic. The lender isn't waiting for you to call. The system monitors the collateral value in real time and executes the sale when the threshold is breached.

By the time you find out, the transaction may already be complete.

Because of the liquidation, the loan is considered paid off.

The Tax Consequences of Liquidation

The IRS does not treat forced liquidation differently from a voluntary sale. When your crypto collateral is sold, that is a taxable disposal event.

You owe capital gains tax on the difference between your original cost basis and the sale proceeds, even though you did not initiate the sale. (See tax code 1.1001-2)

The sale price (the proceeds) is recorded as the outstanding value of the loan at the time of liquidation. If you originally borrowed $100,000 and had paid back $4,000, the proceeds are recorded as $96,000.

That figure is used to calculate your capital gain, regardless of what the collateral was actually worth when the sale occurred.

The result is a tax bill on top of an already painful loss. The crypto is gone.

The prices dropped. And now there is a capital gains liability of potentially 20% to 30% or more, depending on federal rate and state taxes, on assets the borrower no longer holds.

This is the scenario that catches people off guard. The loss feels immediate. The tax bill arrives later.

How Leverage Math Works on a Crypto Loan

Borrowing against crypto creates leverage. Leverage amplifies both gains and losses.

The favorable scenario: Bitcoin averages 15% annual growth. The loan costs 6% in annual interest. The net gain on the position is roughly 9%. The asset appreciates more than the loan costs.

The unfavorable scenario: Bitcoin drops 10% in a year. Add the 6% annual loan cost. The borrower is effectively down 16% on a position they haven't exited. That gap widens with every payment period prices stay down.

Leverage works until it doesn't. The same math that creates the upside also accelerates the downside. Borrowers who don't model both scenarios before entering a crypto-backed loan are only looking at half the picture.

The practical guidance is to pay off crypto-backed loans quickly. Leaving them outstanding for extended periods increases exposure to price volatility.

The longer the loan is active, the longer the collateral is at risk of liquidation.

The Coinbase Mortgage Partnership: What to Know

Coinbase has partnered with Better Homes and Finance Holding Company to allow crypto holders to use their holdings as collateral for a mortgage down payment.

Instead of liquidating crypto to cover the down payment, borrowers take out a loan against their holdings.

The crypto stays. The loan provides the cash.

The practical result is two simultaneous loan obligations: the primary mortgage and the Coinbase crypto-backed loan.

That is a highly leveraged financial position. Both loans must be serviced. The crypto collateral remains at risk for the duration of the second loan.

If crypto prices drop sharply after this arrangement is in place, the borrower faces three simultaneous problems: the mortgage payment, the crypto loan payment, and a potential liquidation event that triggers a capital gains tax bill.

That combination is the worst-case outcome.

Crypto is a speculative asset. It tends to appreciate significantly over long time horizons. In the short term, it is extremely volatile.

Using crypto collateral to fund a mortgage down payment introduces that volatility directly into a major real estate purchase.

This arrangement has legitimate uses. Borrowers with strong conviction about long-term crypto appreciation and sufficient financial cushion to withstand short-term volatility may find it useful.

Borrowers who are already stretched financially should understand the full risk profile before proceeding.

Frequently Asked Questions About Crypto Loan Taxes

|

|

|

|

|

|

|

|

|

|

|

|

|

About CryptoTaxAudit: We're a CPA firm specializing in cryptocurrency tax preparation and IRS representation. Clinton Donnelly (CPA, EA) founded the firm to handle the specific complexities of digital asset taxation that general accountants miss. We've been preparing crypto tax returns since before the IRS had clear guidance, and we stay ahead of emerging issues like crypto-backed loans, DeFi liquidations, and forced disposal events.

Related Articles:How to Cash Out Crypto Safely in 2026: Avoid Bank Freezes, IRS Issues, and Costly Mistakes

Author