The Complete Crypto Tax Compliance Guide for Investors and Traders

By Clinton Donnelly, CEO, Founder | CryptoTaxAudit. Updated 07/15/2026

The IRS uses multiple methods to detect unreported cryptocurrency transactions. These systems work together to build a view of taxpayer activity across exchanges, wallets, and blockchain networks.

Unreported crypto income over $10,000 can result in civil penalties. Willful failure to report may lead to criminal charges.

The IRS uses the following methods to track crypto activity:

- Form 1099-DA reporting: Beginning with the 2025 tax year, U.S. exchanges must report your crypto sales and proceeds directly to the IRS. Coinbase, Kraken, and Gemini will issue these forms to taxpayers. The first reports will show gross proceeds only; cost basis reporting may be added in subsequent years.

- Blockchain forensics: When you transfer crypto between an exchange and an external wallet, the exchange records your blockchain address. The IRS can use forensic tools to trace activity across that address including transactions through DeFi platforms or self-custody wallets.

- AI-powered analysis: The IRS has contracted with Palantir Technologies (at a reported cost of $99 million) to develop systems that identify potential underreporting. These tools analyze trading patterns, social media activity, and other available data to flag returns for review.

- John Doe summons: Federal courts have granted the IRS authority to request customer records from exchanges without specifying individual names. The agency used this mechanism to obtain records from Coinbase, Kraken, and other platforms.

- Crypto-Asset Reporting Framework (CARF): The OECD developed the Crypto-Asset Reporting Framework to enable automatic exchange of cryptocurrency transaction data between participating countries. The U.S. Treasury Department has submitted CARF regulations to Congress and the White House for approval.

- Current status: As of January 2026, this framework remains under review and has not been implemented. If approved, CARF would allow tax authorities to share crypto transaction data across borders, potentially including countries like the U.K., Australia, Canada, and the Netherlands.

PART 1: THE NEW 1099-DA REPORTING REQUIREMENT

Section 1.1: Understanding Form 1099-DA: Digital Asset Reporting Requirements

Beginning with the 2025 tax year, U.S. cryptocurrency exchanges must issue Form 1099-DA to taxpayers. Coinbase, Kraken, Gemini, and Robinhood are among the platforms required to send this form.

DA stands for "Digital Assets." The form reports digital asset taxable events to the IRS, similar to how other 1099 forms report income and transactions.

Form 1099-DA captures sales and transfers, but not purchases, which are not taxable events. If you sold or moved crypto off a centralized U.S. exchange during the tax year, you will receive this form.

What Information Appears on Form 1099-DA

Form 1099-DA provides the IRS with:

- Every crypto sale you execute on the platform

- Every transfer you initiate to an external wallet

- The wallet address where you sent funds

- The asset type and its value at the time of sale or transfer

How Missing Cost Basis Creates Tax Liability Risk

For the 2025 tax year, exchanges will report gross proceeds only. Cost basis will not be included.

Why the Numbers Still Do Not Match Form 8949

The 1099-DA was designed with two goals: to inform the IRS of crypto transactions and to help taxpayers prepare accurate returns. It succeeded at the first and failed completely at the second.

Taxpayers are receiving 1099-DAs that are 20, 30, or even 50 pages long. None of those numbers is a figure they can enter directly on their tax return. The form breaks out transactions in ways that do not map to the line items on Form 8949 or Schedule D.

The IRS compounded this by adding new checkboxes for crypto trading on Form 8949. The result is confusion at every level.

The 1099-DA cannot do that because digital asset transactions require cost basis tracking, and the IRS chose not to require cost basis reporting in the first year of implementation. That decision removed the one piece of information that would have made the form useful.

What remains is a long document reporting transfer activity, purchase dates, and gross proceeds, across dozens of transaction categories, in formats that vary by exchange. Most taxpayers cannot identify what is taxable and what is not just by reading the document.

What Is Form 8949?

Form 8949 is called Sales and Other Dispositions of Capital Assets. It looks like a spreadsheet. This is where you report every crypto sale or exchange.

In each row, you enter what you sold, the dates you bought and sold it, the proceeds, the cost basis, any adjustments, and the net gain or loss.

Page 1 is for short-term gains. These are assets you held for one year or less.

Page 2 is for long-term gains. These are assets you held for more than one year. You can have as many pages of each type as you need.

Some people list every single trade on individual line items. Others enter just the bottom-line totals from all their trading activity.

The IRS accepts it either way.

All your Form 8949 pages get totaled up and flow onto Schedule D. That is where your bottom-line capital gains numbers go on your tax return.

How Do You Fix the 1099-DA on Form 8949?

This is the core of it. You need to do two things on Form 8949:

- First, zero out the wrong numbers from the 1099-DA.

- Second, enter your correct capital gains as calculated by your crypto tax software.

Here is exactly how to do it.

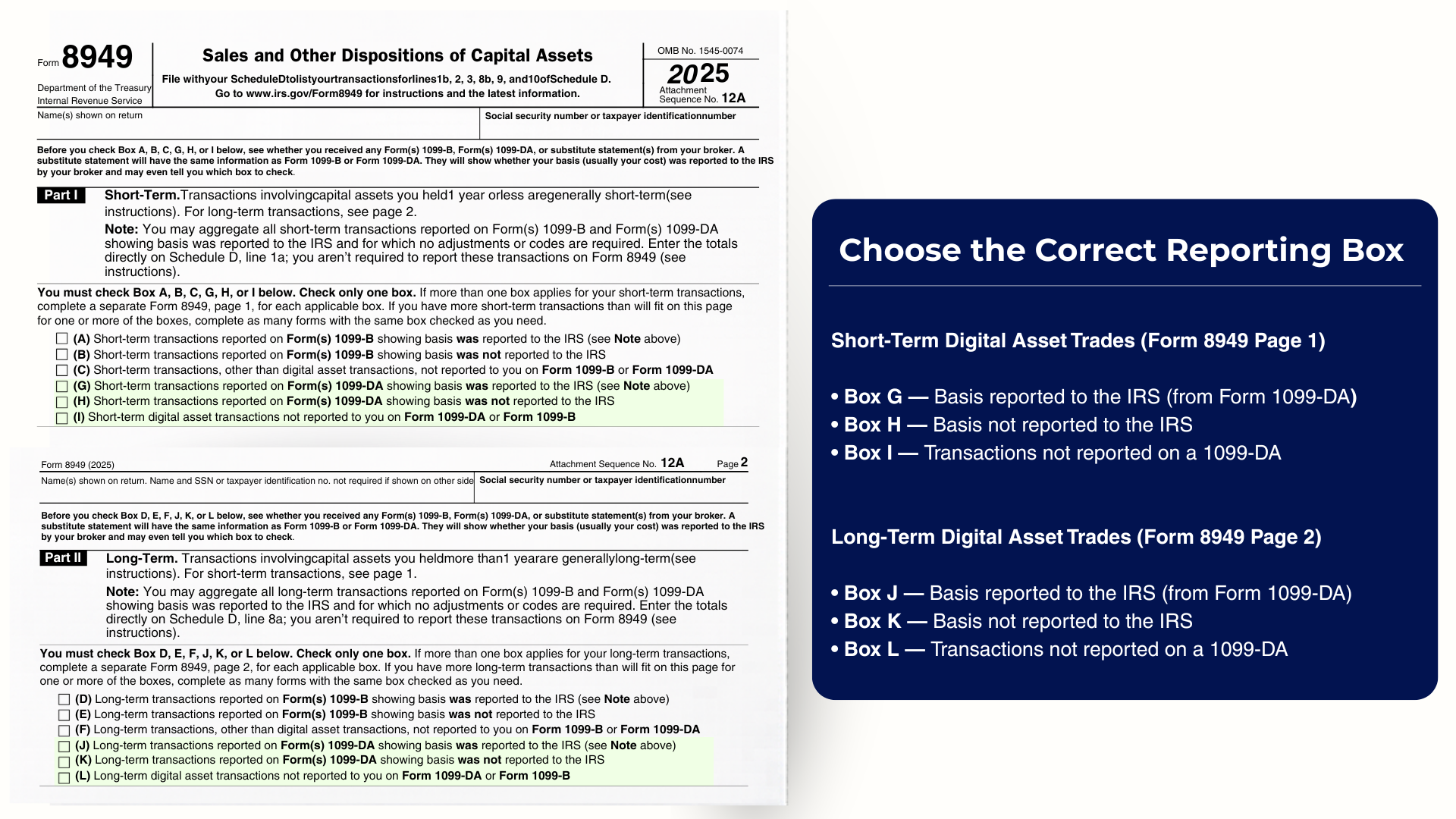

Step 1: Check the Correct Reporting Box

At the top of Form 8949, there is a row of checkboxes. You must check one box to indicate whether cost basis was reported to the IRS on a 1099.

Choose the correct reporting box on Form 8949 based on whether the trade is short-term or long-term, and whether basis was reported to the IRS on Form 1099-DA.

For short-term digital asset trades, the boxes are G, H, or I. For long-term trades, the boxes are J, K, or L.

This year, for your 2025 taxes filed in 2026, most crypto traders will check Box I (short-term) or Box L (long-term).

Why? Because no cost basis is being reported to the IRS on the 1099-DA this year.

Your 1099-DA will tell you whether the transactions are short-term or long-term and whether cost basis was reported. Check the matching box.

In future years, this will change. Some cost basis will be reported, so you will need to check the appropriate box at that time.

Step 2: Zero Out the 1099-DA Numbers

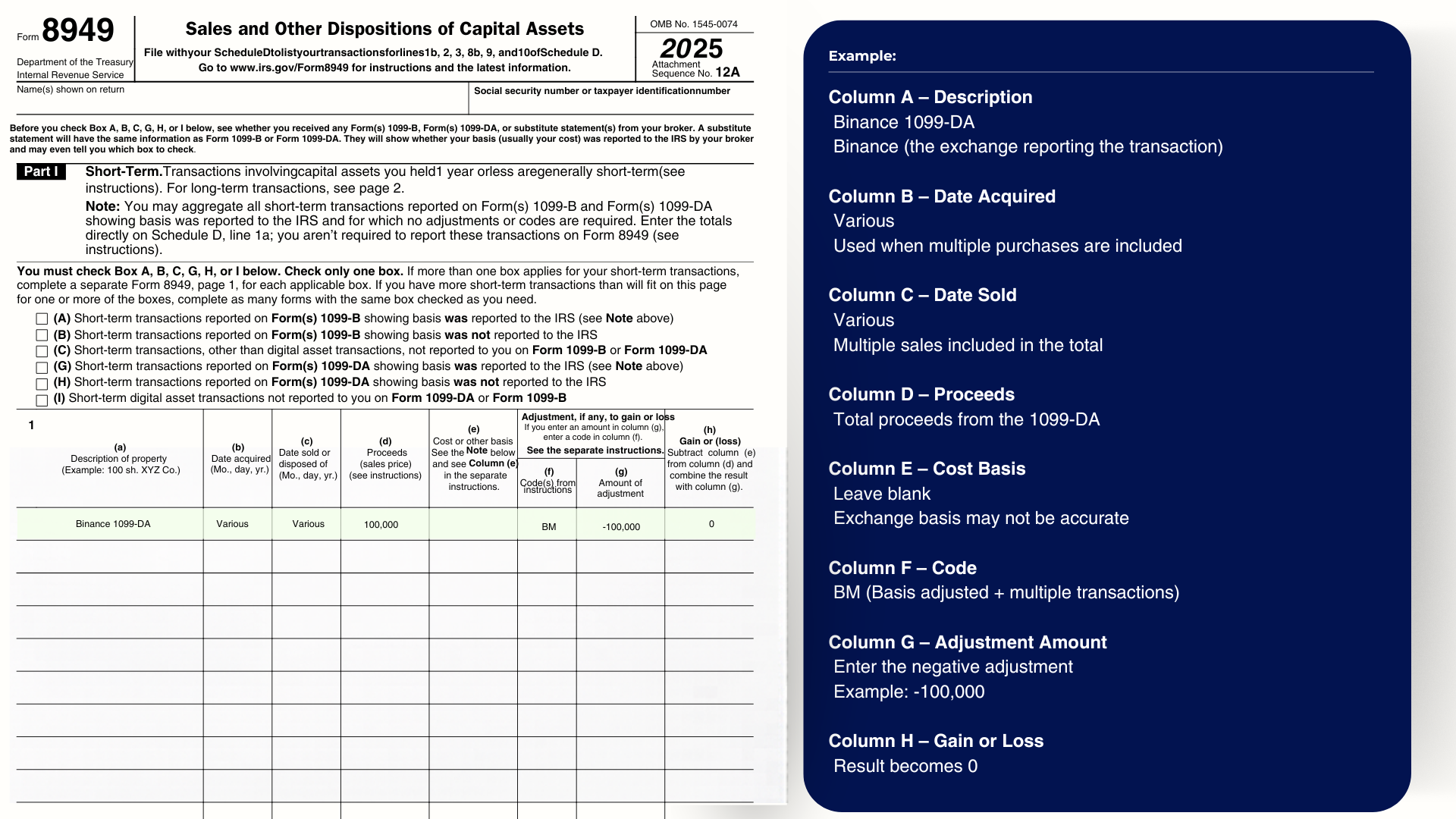

On the first line of the grid, enter the 1099-DA information and then subtract it out. Here is what each column looks like:

Line 1: Enter the 1099-DA amounts and zero them out with a negative adjustment.

Step 2 Breakdown: How to remove incorrect 1099-DA data

- Column A (Description): Write the exchange name and 1099-DA. For example, "Binance 1099-DA."

- Column B (Date Acquired): Write "Various." This is standard when multiple purchases are included in the total.

- Column C (Date Sold): Write "Various." Multiple sales are included in the total.

- Column D (Proceeds): Enter the total proceeds from the 1099-DA for that asset type.

- Column E (Cost Basis): Leave blank. The exchange may not have accurate cost basis, and it is not being reported to the IRS this year.

- Column F (Code): Enter "BM." B means the basis was adjusted. M means the line summarizes multiple transactions.

- Column G (Adjustment Amount): Enter the negative of the proceeds. If the 1099-DA reported $100,000 in proceeds, enter -$100,000 here.

- Column H (Gain or Loss): The result is zero. You have effectively zeroed out the 1099-DA line.

This step accounts for the 1099-DA so the IRS sees you reported it. But it removes the wrong numbers so they do not affect your taxes.

Step 3: Enter Your Correct Capital Gains

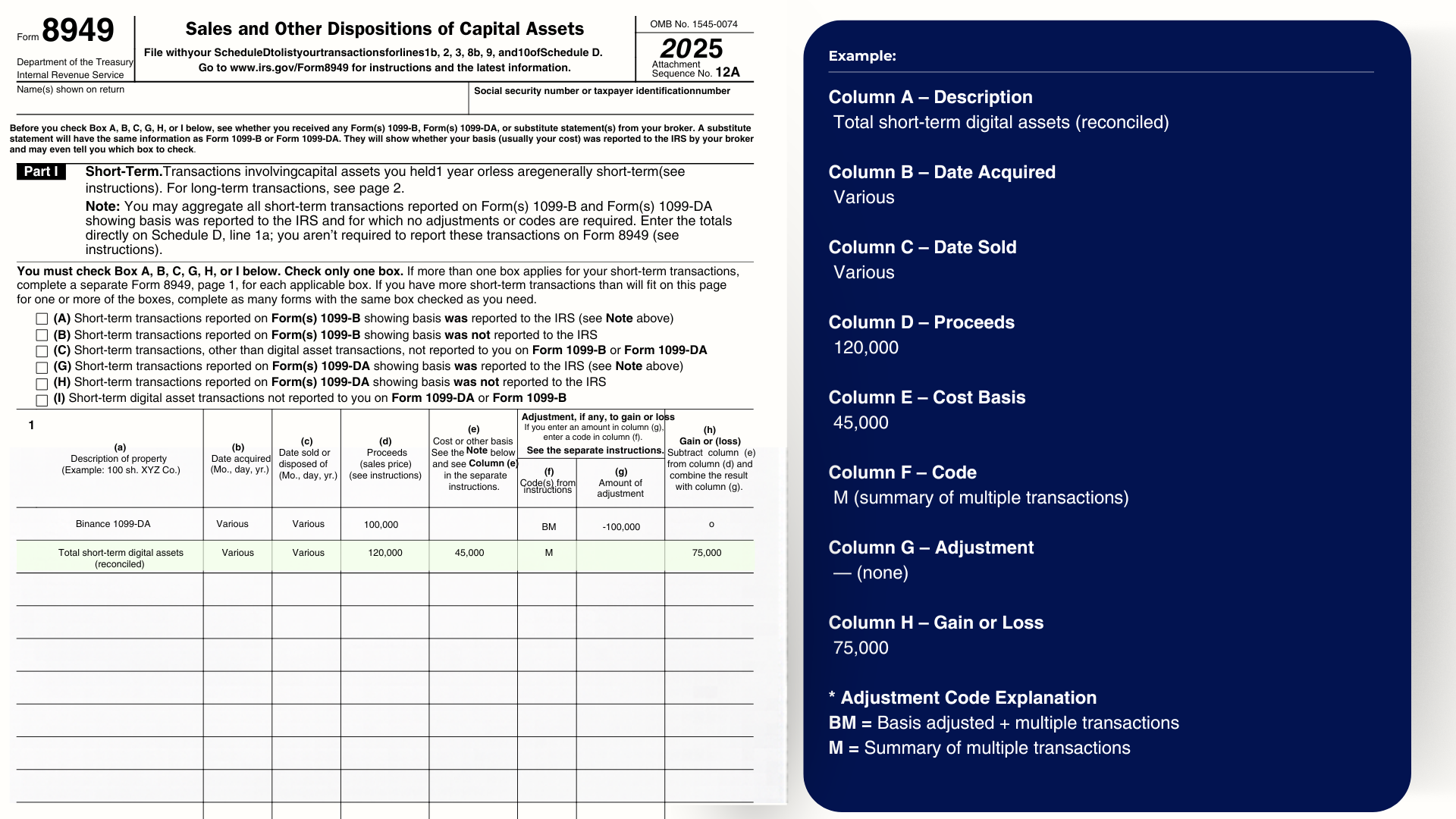

On the next line, you enter the actual capital gains you calculated using crypto tax software like Koinly, CoinLedger, or CoinTracking.

Line 2: Enter your actual calculated capital gains totals.

Step 3 Breakdown: How to report your actual crypto gains

- Column A (Description): Write "Total short-term digital assets (reconciled)" or "Total long-term digital assets (reconciled)."

- Columns B and C (Dates): Write "Various."

- Column D (Proceeds): Enter your total proceeds as calculated by your crypto tax software.

- Column E (Cost Basis): Enter your total cost basis as calculated by your crypto tax software.

- Column F (Code): Enter "M" for summary of multiple transactions.

- Column G (Adjustment): None needed on this line.

- Column H (Gain or Loss): This shows your actual capital gain or loss.

That is how you replace the wrong 1099-DA numbers with the right ones. You account for the 1099-DA and you report your correct gains. Both on the same form.

Need help calculating your crypto gains? CryptoTaxAudit offers Full Service Crypto Gain Calculation. We handle the math so you can file with confidence. Talk to us.

What Happens If You Don't Report Your 1099-DA

If your tax return omits transactions shown on Form 1099-DA, the IRS may issue a CP2000 Notice. This notice proposes additional tax based on the unreported amounts.

You must report all 1099-DA information on your tax return, even if you believe the form contains errors. Discrepancies can be addressed through proper documentation and, if necessary, amended returns.

How a 1099-DA Mismatch Can Trigger a CP2000 or Audit

The IRS receives 1099-DA data from exchanges. It matches that data against tax returns automatically. If a trader's return does not reflect the activity reported on the 1099-DA, the system flags the discrepancy. That can generate a CP2000 notice or escalate to a full examination.

A CP2000 is issued when the income reported on a tax return does not match what the IRS received from third-party sources, including exchanges.

Once an audit is open, the scope expands. IRS agents do not stop at 1099-DA data. They request full transaction histories, a list of all exchanges the trader has used, and supporting documentation for cost basis claims. At that point, decentralized exchange activity comes into the picture.

If the agent discovers significant trading volume on decentralized platforms that was not reported, that becomes the primary audit issue. What started as a 1099-DA mismatch becomes a much larger inquiry into unreported gains.

This is why the off-exchange strategy requires meticulous record-keeping. Keeping assets off centralized exchanges does not protect a trader from audit exposure. It just means the trader has to have their own complete transaction history ready.

PART 2: UNDERSTANDING YOUR REPORTING OBLIGATIONS

Section 2.1: FBAR Compliance for Crypto Holders

Do you need to file? You must file an FBAR if the total value of all foreign financial accounts exceeds $10,000 at any time during the calendar year.

What is FBAR? The Foreign Bank Account Report (FBAR), officially FinCEN Form 114, is a compliance document for individuals with foreign financial interests. The form is managed by the IRS on behalf of the Financial Crimes Enforcement Network (FinCEN).

Filing threshold: The $10,000 threshold is based on the aggregate value of multiple accounts, not a single account.

Why FBAR Is a Powerful Enforcement Tool: U.S. anti-money laundering (AML) laws require U.S. persons to report maximum balances held at foreign financial institutions. Failure to report these balances is subject to substantial penalties.

Reporting maximum balances held at any time during the year is relatively quick and easy for the IRS to prove or disprove. This makes FBAR a powerful enforcement tool.

The penalties can be assessed regardless of whether you reported your crypto income on your tax return. These are separate violations.

Section 2.2: FATCA and Form 8938 Requirements

Do you need to file Form 8938? If your foreign financial assets exceed IRS reporting thresholds (commonly $50,000 for single filers, higher for married couples), you must file Form 8938 with your tax return.

What is FATCA? The Foreign Account Tax Compliance Act (FATCA), enacted in 2010, requires many taxpayers to report specified foreign financial assets on Form 8938. This includes accounts at foreign cryptocurrency exchanges.

Penalties for Non-Compliance: Form 8938 itself does not create tax liability. However, failure to file triggers serious consequences:

- $10,000 penalty for not filing Form 8938 with your original tax return

- $50,000 maximum penalty for continued failure to file after IRS notification

- Indefinitely open statute of limitations on your entire tax return until Form 8938 is filed

- 40% accuracy penalty on any additional tax related to undisclosed foreign assets

- Potential criminal penalties in cases of willful non-compliance

The statute of limitations risk: For early cryptocurrency investors with significant gains, the suspended statute of limitations poses the greatest long-term exposure. The IRS can audit any year for which Form 8938 was not filed, regardless of how much time has passed.

Why Small Transactions Don't Fly Under the Radar

Breaking a large cash-out into many small transactions is called structuring. It's illegal under federal law, and it doesn't work. Banks aggregate small transfers. Ten transactions of $3,000 roll up to $30,000 on the bank's compliance dashboard and trigger the same review as a single $30,000 transfer. The pattern of small, regular transactions from a crypto exchange actually creates more suspicion, not less.

A regional bank manager once put it simply: do one big transaction. One compliance event. One review. One approval. It goes into the records as documented and understood. Multiple small transfers look like someone trying to hide something.

How Tax Compliance and AML Compliance Overlap

Tax compliance and AML compliance draw on the same underlying data: wallet histories, transaction records, cost basis, source of funds, and exchange activity. The difference is the lens applied to that data.

CryptoTaxAudit handles tax compliance. This includes full-service gain calculation, Form 8949 reporting, cost basis reconstruction, and preparation for IRS audits.

Cense handles AML compliance: wallet ownership verification, source-of-wealth documentation, risk scoring, and bank compliance officer engagement.

Banks are also increasingly interested in whether a client is tax-compliant. When someone moves a large sum from crypto to fiat, the bank may wonder whether the transfer is connected to tax evasion. Having both your tax filings and your AML documentation in order removes that question entirely. Running crypto through multiple coin swaps before cashing out generates both suspicious trading behavior and unexpected capital gains. Proper planning with a tax professional and a compliance report prevents both problems.

Section 2.3: Statute of Limitations and Audit Windows

The statute of limitations determines how long the IRS can audit your tax return and assess additional taxes.

Standard audit window: The IRS has three years from the date you filed to audit your return and assess additional tax.

Extended audit window: If you substantially underreported income (defined as underreporting by 25% or more), the statute extends to six years.

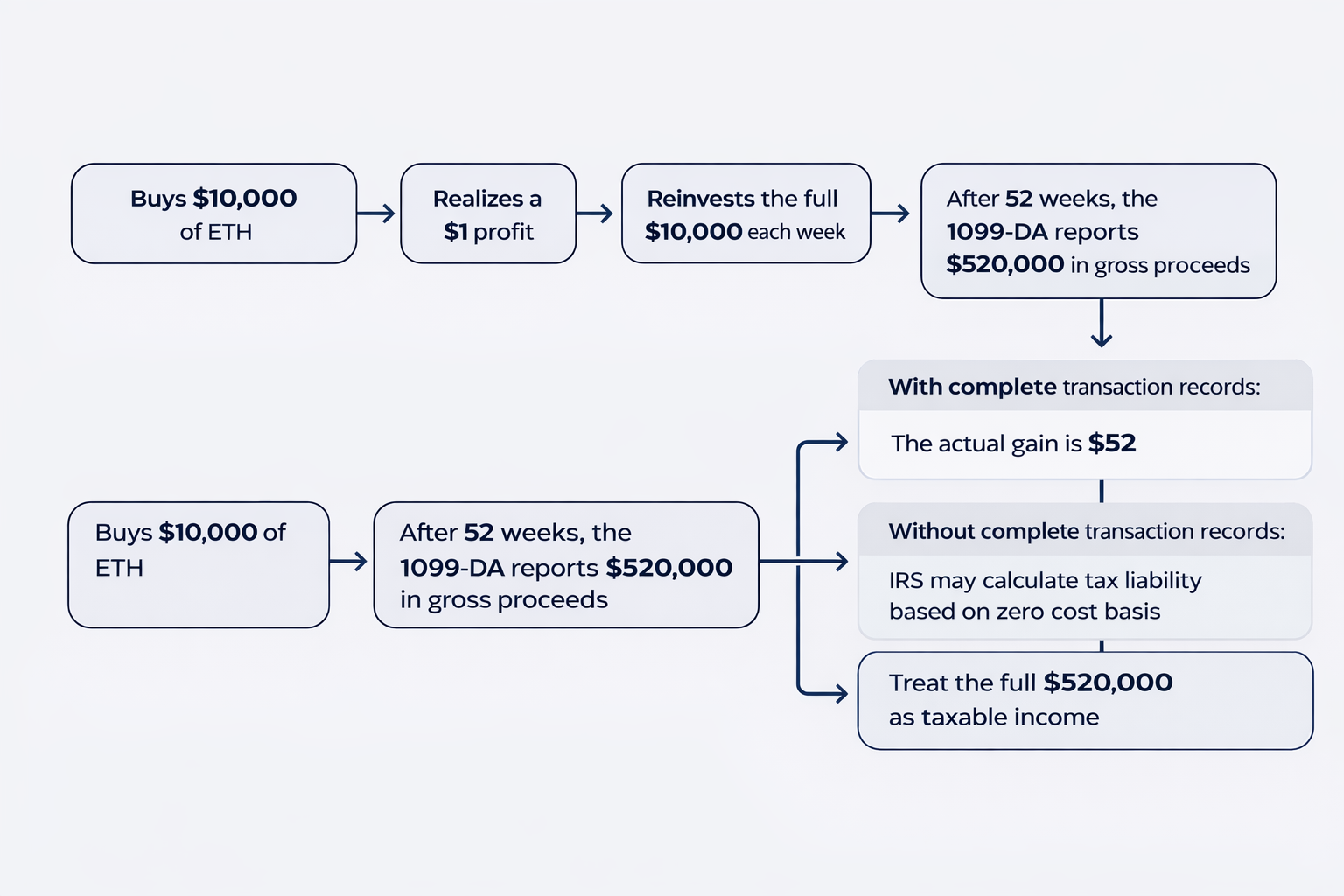

How crypto traders trigger the extended statute:

- Recall the earlier example of a trader who starts with $10,000 and executes weekly trades for a $1 profit each week. The actual annual gain is $52.

- The IRS calculates Total Positive Income (TPI) by adding all sale proceeds. In this example, the IRS sees over $500,000 in proceeds. If the tax return only reports $52 without accounting for the full transaction history, the IRS may conclude you failed to report $490,948 in income, well above the 25% substantial underreporting threshold.

- Proper reporting requires documenting each transaction's cost basis and proceeds, demonstrating how the $500,000 in proceeds resulted in only $52 in net gain.

No statute of limitations for fraud: If the IRS determines fraud occurred, there is no time limit. The agency can audit any year, including years for which you did not file a return.

Section 2.4: Total Positive Income (TPI) and Audit Risk

What is TPI? Total Positive Income (TPI) represents the sum of all sale proceeds without deducting costs or expenses. For IRS audit risk assessment, TPI is the relevant metric, not net income.

How TPI applies to crypto traders: Each time you exchange cryptocurrency for another asset (whether another cryptocurrency, stablecoin, or fiat), the IRS records the sale proceeds. Your cost basis is irrelevant to the TPI calculation.

For high-frequency traders, TPI can reach millions of dollars even when actual profit is minimal or negative. TPI is always positive, even in years when you experienced net losses.

The $400,000 Threshold Misunderstanding: The IRS has stated it will not increase audit rates for taxpayers earning under $400,000. This statement is misleading for cryptocurrency traders.

Most people interpret "income" as net income or adjusted gross income. The IRS uses Total Positive Income for audit targeting purposes.

For cryptocurrency transactions, this means the IRS examines gross sale proceeds, not realized gains. A trader with high transaction volume but minimal actual profit may exceed the $400,000 TPI threshold and face elevated audit risk despite reporting a small net gain or even a loss.

What Is a Liquidation Event?

Liquidation happens when the value of your crypto collateral falls below the lender's required threshold. At that point, the lender sells your crypto automatically to recover what you owe.

You don't make the decision. You don't choose the timing or the price.

The loan agreement defines the liquidation threshold. If you posted $200,000 in Bitcoin to secure a $100,000 loan, you could typically withstand a 50% drop in Bitcoin's price before hitting the liquidation trigger.

Below that threshold, the collateral is sold.

The mechanics are automatic. The lender isn't waiting for you to call. The system monitors the collateral value in real time and executes the sale when the threshold is breached.

By the time you find out, the transaction may already be complete.

Because of the liquidation, the loan is considered paid off.

The Tax Consequences of Liquidation

The IRS does not treat forced liquidation differently from a voluntary sale. When your crypto collateral is sold, that is a taxable disposal event.

You owe capital gains tax on the difference between your original cost basis and the sale proceeds, even though you did not initiate the sale. (See tax code 1.1001-2)

The sale price (the proceeds) is recorded as the outstanding value of the loan at the time of liquidation. If you originally borrowed $100,000 and had paid back $4,000, the proceeds are recorded as $96,000.

That figure is used to calculate your capital gain, regardless of what the collateral was actually worth when the sale occurred.

The result is a tax bill on top of an already painful loss. The crypto is gone.

The prices dropped. And now there is a capital gains liability of potentially 20% to 30% or more, depending on federal rate and state taxes, on assets the borrower no longer holds.

This is the scenario that catches people off guard. The loss feels immediate. The tax bill arrives later.

PART 3: GETTING AND STAYING COMPLIANT

Section 3.1: If You Haven't Reported Crypto in Past Years

Many crypto traders face a compliance gap they didn't intend to create. What started as a small position grew into significant gains, and filing became more complicated each year. The tax liability increased. Time passed.

Understanding how to return to compliance safely requires a clear strategy and proper timing.

Filing Strategy: Start with the Current Year

The most common approach is to file an accurate, complete return for the most recent tax year. This establishes a compliant baseline going forward.

Calculate your crypto gains for the prior six years as well, even if you don't file them immediately. This ensures consistency across all returns and prevents discrepancies if you later file or amend prior years.

A common concern: Won't the IRS question why previous years weren't filed? The electronic filing system accepts returns as submitted without triggering automatic inquiries about prior years. This concern should not prevent you from establishing compliance.

Prepare Past Returns in Advance

Even if you're not ready to file prior years immediately, prepare those returns now. If the IRS initiates contact or your account transcript shows unusual activity, you may need to respond quickly.

Having prior year returns calculated and ready strengthens your position and allows for faster response times.

Why Ongoing Monitoring Matters

The IRS typically flags returns for audit 6 to 12 months before assigning an examiner. During this window, your account transcript may show indicators that a return has been selected for review.

Regular monitoring of your IRS account transcripts can reveal:

- Discrepancies between reported income and third-party information reports

- Returns flagged for future audit before formal contact begins

- Changes to your account that may require immediate response

Early detection provides time to address issues, file amended returns if necessary, or prepare documentation before an audit formally begins. In some cases, proactive correction can prevent the audit entirely or reduce penalties.

Tax Shield by CryptoTaxAudit provides this type of continuous monitoring through a low-cost monthly subscription designed for everyday crypto traders. The service monitors IRS transcripts across all tax years and alerts you to changes that may require action, providing ongoing protection and peace of mind as you navigate compliance.

Multiple Wallets, Multiple Exchanges, One Mess

For investors who used one exchange and one wallet, crypto tax reporting is more work than it used to be, but still manageable.

For investors who used multiple exchanges, multiple wallets, or any DeFi protocols, the complexity compounds quickly. Cost basis must be tracked across every acquisition, disposal, and inter-wallet transfer. Every swap carries a potential taxable gain or loss. The order in which assets are sold affects the tax outcome.

Spreadsheets break down fast. After ten trades across two wallets, tracking cost basis manually becomes unreliable. After a year of active trading across several exchanges, it is not a realistic option.

Good crypto tax software exists, but software is only as accurate as the person operating it. Misclassifying a transfer as a taxable disposal, or missing a transaction that resets cost basis, changes the tax outcome significantly. The tools require expertise to use correctly.

In practice, investors with more than $10,000 in annual crypto gains typically save more through professional gain calculation than the service costs. Professionals know where taxpayers make mistakes, and they correct them before the return is filed.

Secure Your Transaction Records

The burden of recordkeeping falls on the taxpayer. Exchanges may shut down, delete historical data, or become inaccessible. The IRS will not accept missing data as justification for incomplete reporting.

Backup your complete transaction history from every exchange and platform you've used. Maintain a secure copy and document all wallet addresses associated with your activity.

What to Do If You Received an IRS Crypto Notice

If you've received an IRS notice regarding unreported cryptocurrency (including Letters 6173, 6174, or 6174-A), see our guide: Understanding IRS Crypto Tax Notices and How to Respond.

What Is IRS Form 4564?

IRS Form 4564 is an Information Document Request. Agents use it to formally request records from taxpayers during an examination. In crypto audits, a version of this form has been circulated that lists over 100 exchanges, DeFi protocols, and wallet providers.

The audited taxpayer is asked to indicate which platforms they have used. This is a legal requirement. The IRS can compel this disclosure, including under oath in a deposition setting.

The form created significant concern when it became widely known. Privacy-focused members of the crypto community flagged it as overreach. But IRS agents have broad authority to request financial records during an audit, and this form falls within that authority.

The concern most taxpayers should focus on is not whether the IRS can ask. It can. The question is how to respond without creating a legal liability.

Is Form 4564 a Perjury Trap?

The form is only a perjury trap if you sign it without a qualifying statement. The correct approach is to answer under the phrase "to the best of my knowledge." That language is meaningful.

If it turns out later that you forgot an account, the qualifier gives you room to correct the record. A taxpayer might recall years after a transaction that they held funds on an exchange like BitConnect, or had assets stuck on a platform they couldn't access. The "best of my knowledge" language means an incomplete answer at the time of signing is not automatically perjury.

This is a standard legal qualifier used across many types of sworn statements. It reflects the reality that memory is imperfect, especially over multi-year trading histories across dozens of platforms.

Answer the form. Use the knowledge qualifier. That is the way through it.

Key Compliance Points Every Crypto Trader Should Understand:

- Form 1099-DA reports gross proceeds only for the 2025 tax year. You must document your cost basis separately to prove actual gains.

- FBAR filing is required if the aggregate value of foreign financial accounts exceeds $10,000 at any point during the year. Penalties apply regardless of whether you reported crypto income correctly.

- Total Positive Income (TPI), not net income, determines IRS audit targeting. High transaction volume can exceed the $400,000 threshold even with minimal actual profit.

- Substantially underreporting income by 25% or more extends the audit statute from 3 years to 6 years. Crypto traders commonly trigger this through incomplete transaction reporting.

- The IRS flags returns 6 to 12 months before assigning an auditor. Early detection during this window can prevent audits or reduce penalties.

PART 4: PROTECTION AND PROFESSIONAL SERVICES

Section 4.1: Understanding Audit Defense

If the IRS initiates an audit, the timeline typically extends two to four years from initial contact to resolution.

Crypto audits require recalculating transaction histories, documenting cost basis for thousands of trades, and challenging the IRS's proposed adjustments.

Initial representation often requires $10,000 to $50,000 upfront. Total defense costs can exceed $150,000 for cases that proceed through examination, appeals, or Tax Court. Most taxpayers significantly underestimate both the duration and total expense involved.

The Proactive Approach

The most effective audit defense begins before the IRS makes contact. The agency typically flags returns for audit 6 to 12 months before assigning an examiner. During this window, early detection and correction can prevent the audit entirely or significantly reduce penalties.

Tax Shield by CryptoTaxAudit provides this proactive protection through continuous IRS account monitoring and full audit representation coverage. Designed as an accessible entry point for crypto traders

Tax Shield includes:

- ✓ Continuous monitoring of IRS transcripts across all tax years

- ✓ Initial risk review to identify potential compliance issues

✓ IRS audit representation if an examination begins

✓ Letter review and response for IRS notices

✓ FBAR filing assistance

✓ Ongoing support from crypto tax specialists

Unlike reactive audit defense (which can cost $10,000-$50,000 upfront when the IRS makes contact), Tax Shield provides ongoing protection through a monthly subscription. This approach allows traders to stay ahead of IRS scrutiny rather than scrambling after receiving an audit notice.

Section 4.2: Professional Tax Preparation and Gain Calculation

DIY crypto tax software serves a specific purpose. For investors who buy and hold a few assets on one or two U.S. exchanges, these tools can generate adequate results.

However, certain situations require professional expertise:

- Complex transaction histories: High-frequency traders, DeFi participants, and those using multiple exchanges face calculation challenges that automated software often cannot resolve accurately. Transaction volumes in the thousands or millions require specialized reconciliation methods.

- Foreign exchange activity: Accounts at non-U.S. exchanges trigger FBAR and FATCA reporting requirements beyond standard tax return preparation. Missing these filings creates penalties separate from any tax liability.

- Advanced DeFi protocols: Liquidity pools, yield farming, staking rewards, and wrapped tokens involve tax treatment questions that remain unsettled or poorly documented. Incorrect classification can result in substantial overpayment or underreporting.

- Compliance gaps from prior years: Returning to compliance after periods of non-filing requires strategic planning. The approach differs significantly from routine annual filing.

Why DIY Crypto Tax Software Overstates Your Gains

These platforms aren't trying to rip you off. They're just not built to optimize. They're not built to minimize your tax bill. They're built to automate calculations.

| Issue | DIY Crypto Tax Software | CryptoTaxAudit Full Service |

|---|---|---|

| Cost basis matching | When you have multiple buys at different prices, the order you sell them matters. A lot. DIY software uses default methods that often inflate gains. | We use the method that legally minimizes your tax bill. |

| Wallet-to-wallet transfers | Move Bitcoin from Coinbase to your hardware wallet? That is not taxable. But if software does not see both sides, it treats it like a sale. Instant phantom gains. | We reconstruct both sides so non-taxable transfers stay non-taxable. |

| Staking rewards | Some platforms count the initial receipt as income and then count it again when you sell. | We separate income and capital gains correctly so nothing is double-counted. |

| DeFi transactions | Provide liquidity? Swap tokens in a pool? DIY software often cannot parse what actually happened. It guesses. And it guesses high. | We manually review the activity to determine what actually happened. |

| Missing data | If you cannot import a wallet perfectly, many platforms skip it or make assumptions that favor reporting more income, never less. | We use blockchain analysis to properly reconstruct missing transactions. |

We optimize for the lowest legal tax bill. That's the difference.

CryptoTaxAudit Services

Crypto gain calculation: Accurate calculation of taxable gains across all transaction types, including complex DeFi activity, high-volume trading, and multi-year reconciliation. This service works as a standalone calculation or integrates with your existing tax preparation.

Tax return preparation: Complete tax return preparation using methods designed to withstand IRS scrutiny. This includes proper reporting of all digital asset income, required disclosure statements, and FBAR/FATCA compliance where applicable.

For more information: Crypto Gain Calculation Services | Tax Return Preparation

Author