A Practical Guide to Crypto Theft, Scams, and Tax Loss Deductions

By Clinton Donnelly, CEO, Founder | CryptoTaxAudit

Crypto scams are increasing every year. Investors lose funds through theft, phishing attacks, romance scams, and fake exchanges.

For many investors, the next question is whether any of that loss can be reported on a tax return and what documentation the IRS may require.

This guide explains how these scams work and how the IRS treats crypto losses when they occur.

Crypto Theft Tax Losses: What the IRS Lets You Deduct and How to Prove It

How Much of a Stolen Crypto Loss Can You Write Off on Your Taxes?

With all these losses, you can only recover your basis. That's what you put into the investment.

You cannot recover the fair market value of the investment at the time the loss occurred. Track your basis carefully and keep records that show what you originally paid.

Do You Need a Police Report to Claim a Crypto Theft Loss?

Yes. First thing after a theft: file with the FBI Cyber Crime Unit. File with local police if they'll take the report.

Get case numbers. Get copies of everything. The police will take your report.

They'll write down the wallet address where your Bitcoin went. Then they'll tell you there's nothing they can do.

The wallet's in Moscow or Singapore. Your coins are gone. But you need that police report number for the IRS.

That's the only reason you're filing it.You should keep the report number and supporting records with your tax documentation.

Does a Crypto Phishing Scam Count as Theft on Your Tax Return?

Yes, if it qualifies as theft under your state law. You'll need evidence you were deceived and didn't willingly transfer the coins. Whether it qualifies depends on the facts, the documentation, and how the transfer occurred.

You Got IRS Letter 3176C After a Crypto Theft Claim. Now What?

The IRS sends Letter 3176C. It says your claim looks frivolous.

You have 30 days to send proof or they'll disallow the deduction.

If it's a significant loss, expect a letter.

You need documentation ready before you file. You'll need FBI reports, police reports, and basis records.

These cases usually require organized documentation and a timely response.

How Much Can You Deduct If You Lost Crypto in a Ponzi Scheme?

You can deduct your actual cost basis, not the inflated returns the scammer showed you. Your statement showed $100,000.

You think you're claiming a $100,000 loss. But you only put in $10,000.

The rest was fake returns the scammer made up.

The IRS gives you $10,000. That's your basis.

The fake $90,000 in "gains" doesn't count. They will give you credit for your cost basis.

That's it. Ponzi-related losses usually require careful documentation and the correct reporting method.

What Does the IRS Do If You Recover Crypto You Already Claimed as a Loss?

If you get a refund later, the excess has a zero cost basis.

You already claimed it as a loss, so you treat the recovery as having zero basis.

Any recovered value is taxable. Recoveries need to be reported carefully because the prior loss treatment affects the tax result.

Can You Deduct Crypto That Was Stolen in a Home Invasion?

Yes. Section 165 talks about losses.

Section C breaks down three types: business losses, investment losses, and personal losses.

An investment loss is defined as an activity engaged in for profit.

Crypto held for investment qualifies as an investment loss under IRC Section 165(c)(2).

If you had coins stolen, you can claim that loss on Form 4684.

You write it off as a type of itemized deduction where you report casualty and theft losses.

These claims are documentation-heavy, so records should be organized before filing.

Need Help Reporting a Crypto Theft Loss?

Crypto theft tax reporting can be complicated, especially when dealing with police reports, IRS verification letters, and basis calculations.

The team at CryptoTaxAudit helps investors review their situation, document losses properly, and prepare filings that accurately reflect what happened.

Pig Butchering and Crypto Romance Scams: How They Work and What You Can Claim

What Is Pig Butchering in Crypto?

A stranger strikes up a conversation, friendly, flirty, sometimes even spiritual.

Over time, they build trust, sometimes over weeks or months.

Then comes the pitch.

Whether it's framed as romance or opportunity, the result is the same: emotional leverage.

That leverage is used to extract real money from people who often don't realize they've been conned until they're $50,000 or $500,000 too deep.

They call it pig butchering. Not because it's subtle, but because it's slow, calculated, and devastating.

How Do Crypto Romance Scams Actually Work?

These fake platforms often show unrealistically high growth, 20% monthly returns, rapid compounding gains, and screenshots of fake account dashboards.

Victims can even "withdraw" small amounts early on, reinforcing the illusion of legitimacy. But as more money goes in, suddenly, withdrawals get blocked.

"There's a tax you need to pay first." "We're having processing issues." "Just one more step."

Just when victims start to realize they've been duped, the scammers go for one last cut.

"To get your $250,000 out, you need to pay a 20% tax, just $50,000 more."

Desperate to salvage something, victims often send it.

And then? Silence.

Can You Claim a Tax Loss If You Were the Victim of a Pig Butchering Scam?

Victims of these scams may be able to claim an investment theft loss.

That means if you lost $110,000 to one of these schemes, and you're in a 30% combined tax bracket, you could potentially reduce your tax burden by $33,000.

No, it doesn't make you whole.

But it's better than walking away empty-handed.

Most CPAs and TurboTax wizards have no idea how to handle these cases properly.

You need a firm that specializes in crypto fraud and understands how to document these losses correctly under IRS rules.

If someone is indicted for operating a pig butchering scam, you can utilize the Ponzi scheme treatment found in tax form 4684, part C.

This allows you to deduct the principal amount you invested, excluding any artificial growth, on your current year's taxes under Schedule A.

What If No One Is Indicted in Your Crypto Scam Case?

In many cases, the absence of an indictment limits your options.

Here, you can report the loss as a capital loss using tax form 8949.

This document serves as a detailed record of your transactions, listing the original investment as the purchase price and $0 as the selling price.

This approach enables you to offset the loss against capital gains.

What Documentation Does the IRS Need to Prove a Crypto Scam Loss?

The IRS requires substantial documentation to support your claims.

According to tax code section 6001, the onus is on you to prove any losses sustained.

You should consider maintaining thorough records of all related transactions.

A police or FBI report can be helpful, as can employing a forensic investigator to trace and verify the transfers to the fraudulent wallet involved.

Given the permanent nature of blockchain records, this evidence could prove invaluable during an audit.

How Does CryptoTaxAudit Help Pig Butchering Scam Victims?

CryptoTaxAudit offers expert guidance on how to handle scam-related losses on your taxes, including deduction strategies, IRS forms, and audit-ready documentation.

CryptoTaxAudit does not offer fund recovery or legal enforcement services.

AI-Powered Crypto Scams: How to Spot Them and Report Losses to the IRS

How Do You Report a Crypto Rug Pull Loss on Your Taxes?

If the loss resulted from an investment in a scam coin or 'rug pull', you should be able to deduct such losses even if the asset has no liquidity and you can no longer sell (therefore realizing a taxable exchange).

If you can sell the asset, even at a fraction of your cost, you would report this loss as any other crypto loss on IRS Form 8949.

In cases where you can no longer sell the tokens, it is possible to use a burn address, disposing of the tokens for $0; in this case, the loss would also be reported on IRS Form 8949.

How Do You Report Abandoned Crypto on Your Tax Return?

In instances where you've abandoned a business or investment asset, you'd report this loss on IRS Form 4797, line 10.

This form is typically used to report the sale or exchange of property used in a trade or business (Section 1231 property), but it also has provisions for reporting the abandonment of property.

Can You Deduct Stolen Crypto If It Was Business or Income-Producing Property?

Investments in cryptocurrencies could be considered income-producing property; however, no guidance has been provided by the IRS. It's important to note that the rules are more restrictive for personal property due to the TCJA changes.

For losses due to the theft of business or income-producing property, you would use IRS Form 4684, Section B.

The term 'business or income-producing property' generally refers to property used in a trade or business or for the production of income.

This would typically include business assets such as machinery and equipment, buildings, vehicles, other business property, and investment properties like rental real estate.

Therefore, if you have sustained substantial losses, we recommend consulting with a tax professional to understand the options for deducting such losses.

Is There a Specific IRS Provision for Crypto Ponzi Scheme Losses?

If you've been a victim of a Ponzi-type investment, the tax code offers a specific provision under Rev. Proc. 2009-20, which allows for a potential deduction.

However, the safe-harbor rules require you to meet certain criteria, which typically include an indictment or formal complaint being filed against the scheme's perpetrators.

These losses are reported on Form 4684, Section C.

How Does AI Make Fake Crypto Exchanges Look Real?

The name of the game when it comes to crypto investment scams is the appearance of legitimacy.

No matter the variant of the scam, the victim needs to feel like the website or advertisement they are directed to is the real deal.

Before AI, scammers did their best to emulate the look and feel of a legitimate exchange.

A keen observer, however, would still be able to spot inconsistencies and errors within the content.

AI website generators can bypass this with immaculate and professional-grade pages.

Additionally, if a scammer hopes to impersonate an existing exchange, they can do so with relative ease to catch more victims off guard.

Advertisements and calls to action benefit heavily from AI-generated content as well.

With the use of deepfake technology, scammers can use existing content from big names and tailor it to their narrative (if you haven't seen an Elon Musk crypto scam video, you're bound to sooner or later).

Can You Tell If a Crypto Investment Video Is a Deepfake?

Watch the mouth movements and make sure the language matches the lips with clear resolution.

When it comes to deepfakes, a lot of the same principles from romance scams still apply.

The problem with spotting AI generated fake exchanges is that they're just too good.

While a small error or inconsistency may be lurking in the website, they could be too small to pick up immediately.

What Is the Simplest Way to Avoid an AI-Powered Crypto Investment Scam?

The simplest way to avoid this is to not click on the link someone sends you.

Instead, find it independently.

If it sounds too good to be true, it probably is.

Stay away from private groups.

For all you know, every user could be part of a group who are carefully trying to lower your guard. It might even be the same person controlling multiple accounts.

If someone contacts you and brings up crypto investing, don't take them for their word.

See if what they say passes the sniff test of friends, family, or colleagues.

If you don't know anyone familiar with crypto, take your question to threads like r/CryptoScams and see what they have to say.

While you may not be able to readily spot an AI generated scam website, you can still pay attention to exchange domains.

When it comes to imposter sites, don't assume they are legitimate if there are similarities to the name.

While the future of crypto is bright and potentially lucrative, it does not mean easy money.

When it comes to exchanges you've never heard of but are recommended by the other person, simply turn tail and run.

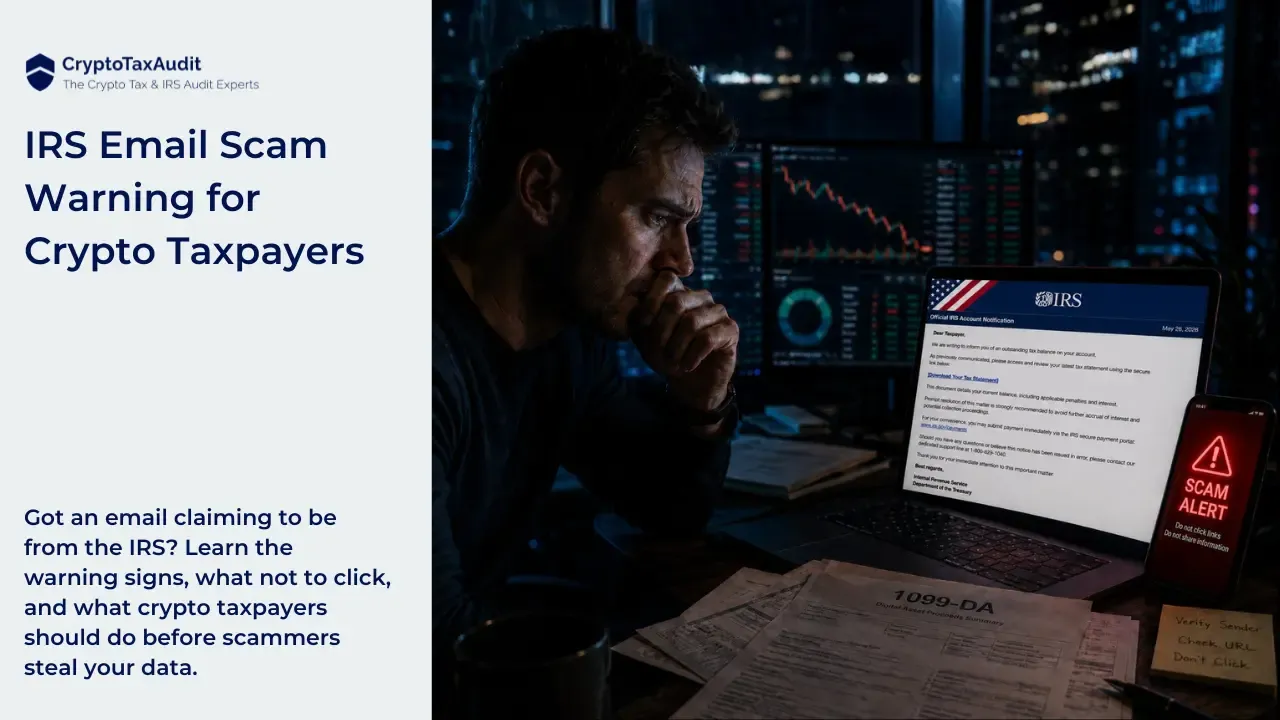

How Are Scammers Using AI to Phish Crypto Holders?

Thanks to countless data breaches, scammers may already have your phone number and/or email address, complete with knowledge of potential accounts you associate with it.

From there, it's just a simple poke and prod with misleading notices meant for you to take action by clicking on the link they provide, of course.

Once they gain access to your account, they can gather even more sensitive information or use the access they have to drain your balance.

Phishing attacks represent a pervasive and insidious form of cybercrime, designed to exploit human psychology rather than technical vulnerabilities.

Typically carried out through deceptive emails, messages, or websites, phishing seeks to trick individuals into divulging sensitive information such as login credentials, financial details, or personal data.

How Do You Spot an AI-Generated Crypto Phishing Email?

It may be a sobering thought, but you cannot trust anything sent to you.

Regardless of how legitimate that email or text message may look, you have to assume that it could be a trap.

Scammers will often use official communications from platforms and mirror them perfectly.

Just like the fake exchanges highlighted above, phishing emails and texts can be extremely deceptive when generated by AI.

Pay attention to the sending email address, and see if it matches earlier known official communications.

Your best bet is to spot any grammatical or spelling errors around portions of the message that relate to clicking on links or the given reason for reaching out to you in the first place.

If a company or service reaches out to you to give notice or instructs you to take action, it is best to contact the provider directly for confirmation.

This means using publicly available contact information and NOT what is listed in the message.

How Is AI Making Crypto Scams Harder to Detect?

AI can generate live video to accompany the fake voice and carry full conversations, which only lowers the victim's guard further and builds on the lie.

This goes well past voice calls as well. Now, scammers can use AI-generated voices to not only match the sex, but the age and region in which their victim resides.

AI tools can clone voices, generate deepfake videos, and build professional-looking websites that mimic real exchanges.

This makes it much harder for investors to tell what's real and what's fake.

Are Crypto Scam Losses Tax-Deductible Under Current IRS Rules?

The key question is whether cryptocurrency is, in fact, personal property or business and income-producing property.

The Tax Cuts and Jobs Act of 2017 (TCJA), significantly changed the deductibility of losses arising from theft or scams of personal property.

Casualty losses of personal property are currently limited to losses caused by a federally declared disaster until 2025.

However, personal property losses are generally not deductible under the Tax Cuts and Jobs Act.

If the scam involves business or income-producing property, you may be able to claim losses using IRS Form 4797 or 4684. In some cases, yes.

Always consult a crypto tax professional to review your case.

What Is the Best Defense Against AI-Powered Crypto Scams?

A healthy dose of base skepticism is going to be your best tool in keeping safe.

If it sounds too good to be true, it usually is.

Never take an unsolicited message at face value, and always consider what a bad actor stands to gain from clicking that link or answering that text.

Verify exchange domains independently and be cautious of anyone promising guaranteed returns.

Never trust links or private groups sent by strangers.

How Can CryptoTaxAudit Help After a Crypto Scam Loss?

If you've been the victim of a crypto scam or lost funds in a rug pull, CryptoTaxAudit can review your tax options, calculate your losses, and defend you in the event of an audit.

CryptoTaxAudit can assess whether your losses may qualify for tax reporting, defend your filings in the event of an IRS audit, and provide forensic support through partners like CoinStructive.

Our team specializes in crypto gain calculations, IRS audit protection, and ongoing IRS monitoring.

Celsius Bankruptcy: How to Report Losses, Distributions, and Clawbacks

What Happened With Celsius and Why Does It Affect Your Taxes?

Celsius investors have encountered a rollercoaster of events that not only impacted their portfolios but also introduced complexity to their tax filings.

From Celsius’s closure and bankruptcy filing in 2022 to the indictment of Alex Mashinsky in early 2023 and subsequent payouts in 2024, understanding how to report these events on tax returns has become crucial.

Because these events spanned multiple tax years, they add another layer of complexity to an already intricate tax preparation process.

Mashinsky was later sentenced to 12 years in prison for fraud. The sequence of events surrounding Celsius has left many investors wondering how to report their losses accurately.

Can Celsius Investors Claim a Ponzi Scheme Loss on Their Tax Return?

Investors can use Form 4684 Part C to claim a tax fraud loss, leveraging the safe harbor provision. This doesn't require proof beyond the indictment.

However, this is capped at 75% of the invested amount.

But, since the actual loss is about 30%, the taxpayer would have to treat the difference as income, making this a messy approach.

What Is the Cleanest Way to Report a Celsius Bankruptcy Loss?

This is the cleanest way to report the loss. Since the payout was in 2024, the loss is claimed on the 2024 tax return, which was filed in 2025.

The Celsius bankruptcy administrator issued a 1099 form in January 2025, which made the tax filing easier.

Additional distributions were made in November 2024, August 2025, and February 2026. How each distribution is reported depends on the method used to claim the original loss.

For many, the cleaner and more defendable route is to report the loss directly related to the bankruptcy, avoiding the potential overstatement of losses and the need to adjust future tax filings.

This approach not only simplifies the reporting process but also aligns closely with the actual financial outcome for investors.

What Is a Celsius Clawback and Who Does It Apply To?

The clawback applies to people who withdrew capital in excess of $100,000 from Celsius within 90 days of its declaring bankruptcy.

Clawback is an informal term for what the law calls preferential payments.

The concept is that preferential payments are given to people who had the inside scoop that things were getting bad and took their money out because they had gotten insider information.

So if you benefited from that insider information, you owe it back to all the other creditors who did not have that information. This is the legal argument behind the clawback.

What If You Withdrew From Celsius Based on Public Information, Not Insider Knowledge?

For many who withdrew their investments from Celsius, the decision was based on publicly available information and the visible signs of the company's declining stability, not insider knowledge.

This stance poses a significant challenge for the Celsius administrators, who must prove that an investor had acted upon insider information to justify a clawback.

What Are the Tax Consequences of Paying or Refusing a Celsius Clawback?

Investors confronted with a clawback request face a complex scenario that intertwines legal and tax considerations.

Paying a clawback can lead to reporting a capital loss on tax returns.

If you do pay a clawback, then that's an additional capital loss on that transaction, which you report in Form 8949.

Refusing to pay, based on the argument of not having insider information, carries its own set of implications and requires a strong legal stance.

If you don't pay the clawback, then there's no impact on your tax return.

How Does CryptoTaxAudit Help Celsius Investors?

At CryptoTaxAudit, we understand that every Celsius investor’s situation is different. Some investors received distributions, others faced clawback demands, and many are unsure how to report their losses correctly.

Our team helps investors review their specific situation, determine the correct tax treatment, and prepare filings that accurately reflect what actually happened with their Celsius holdings.

If you need help reporting Celsius losses or distributions, you can learn more here.

Key Takeaways From This Guide

- Crypto held for investment qualifies as an investment loss under IRC Section 165(c)(2).

- With all these losses, you can only recover your basis. That's what you put into the investment.

- The IRS requires substantial documentation to support your claims.

- Scam losses may qualify depending on how the funds were transferred.

Related Articles: The Complete Crypto Tax Compliance Guide for Investors and Traders

Author